Blogs

Budget 2025: What you need to know about salary sacrifice changes

After months of speculation about what Rachel Reeves’ Budget would hold for pensions, we now have answers.

Published on 28th November 2025

|

4 min read

The headline announcement is as previously trailed: a £2,000 annual cap on salary sacrifice pension contributions will be introduced.

While this sounds like a big change, the reality is much more reassuring for employers. For starters, the changes won’t come in until 2029 – so there’s plenty of time to prepare. What’s more, salary sacrifice – or salary exchange, to use its friendlier name – remains one of the most valuable benefits you can offer your employees.

Here's everything you need to know.

What did Rachel Reeves announce about salary sacrifice on pension contributions?

The Budget confirmed that from April 2029, employees will still be able to pay their contributions via salary sacrifice but up to a maximum of £2,000 per employee, per year.

This means the first £2,000 of each employee’s salary-sacrificed contributions will still enjoy full NIC savings, exactly as they do today. It’s only contributions above this threshold that will be subject to NICs.

Crucially, normal employee pension contributions that aren’t made through salary sacrifice will remain unaffected by these changes.

What do these changes mean for employers right now?

The good news is that these changes aren’t due to come in until April 2029. So, for now, you can continue to benefit from the current system. There’s no need to make changes to your existing salary sacrifice arrangements or worry about any immediate compliance issues.

Should you start using salary sacrifice for your workplace pension if you don’t already?

Our view is: absolutely. Between now and April 2029, you and your employees can enjoy the full NIC savings on all salary sacrifice contributions. And even after the £2,000 cap comes in, salary sacrifice will still deliver a lot of value.

Setting up salary sacrifice can feel complicated, but at Cushon, we make it easy. We take care of all the heavy lifting – including payroll integration, supplying the templates needed, as well as educational content for your employees so they understand all the benefits. You can start saving without any admin headaches – all at no extra cost to your business.

How much could you save through salary sacrifice, as an employer, in the next three years?

Here are some examples based on a typical 5% employee contribution rate:

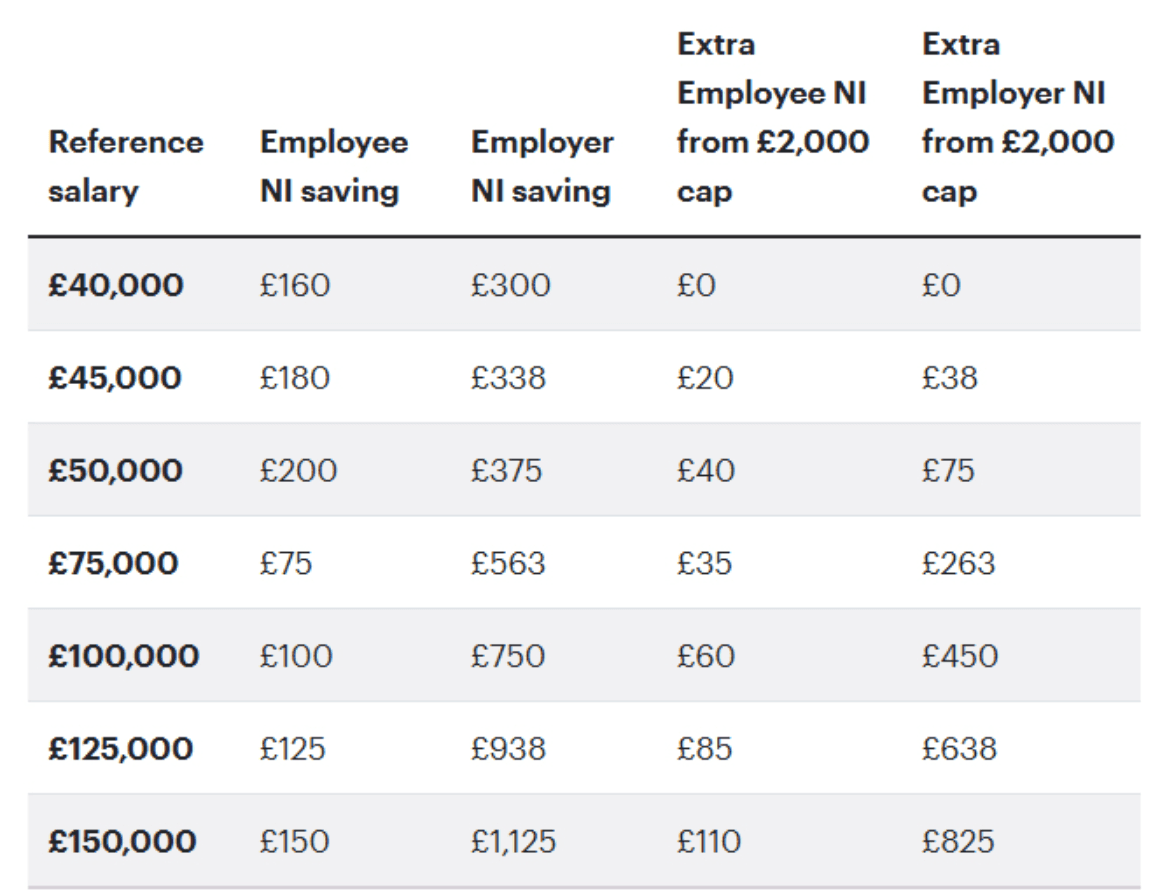

£40,000 salary: £460 total annual saving (£300 employer, £160 employee)

£75,000 salary: £638 total annual saving (£563 employer, £75 employee)

£125,000 salary: £1,063 total annual saving (£938 employer, £125 employee)

For a company with 50 employees on an average salary of £40,000, that’s £23,000 per year in savings – nearly £70,000 up to April 2029.

It’s worth noting, too, that some employers choose to reinvest their NIC savings into boosted pension contributions, giving employees better retirement outcomes at no extra cost.

To find out exactly how much money your company could be saving annually, try using our salary sacrifice calculator.

What will the impact be when the £2,000 cap kicks in from April 2029?

For most employees, the impact will be minimal. Here’s what it looks like for 5% employee contributions:

Up to £40,000: No change – contributions stay within the £2,000 threshold

£75,000 salary: Around £35 less in NIC savings for employees, £263 less for employers

£125,000 salary: Around £85 less in NIC savings for employees, £638 less for employers

The table below, from the Office of Budget Responsibility report, shows the current NI savings available for employee and employer, and how these will change after April 2029.

Annual savings from salary sacrifice, and effect of a £2,000 cap, where employees sacrifice 5%

Table assumes current NI rates still apply after the Budget.

The key takeaway is that every employee using salary sacrifice will still benefit from NIC savings on the first £2,000.

Book a free review of your pension scheme

Want to learn more about how your business could benefit with salary sacrifice? Get in touch with our team today to arrange a free review of your workplace pension arrangements. We’ll show you exactly how much you and your employees could save – now and into the future.

This commentary on the 2025 Budget was produced on 27 November 2025. All references to tax treatment refer exclusively to UK taxation, based on our current understanding of UK laws and HMRC practices as of this date. Tax reliefs may change in the future and are not guaranteed.

You may also like

Blogs

Pensions dashboards allow you to see all your pensions in one place

All the pensions you’ve ever had, all in one place. Coming soon to help you take control of your financial future.

Cushon

Blogs

Investments the missing link in pension engagement

Every September, campaigns remind us to ‘pay more attention’ to our pensions – proof, if anything, that employees are still disconnected from what is often their most valuable workplace benefit.

Steve Watson, Director of Policy & Research

Investment impact

Putting money where it's fit for the future

Unless you make your own investment decisions, your pension savings will be invested according to our Cushon Sustainable Investment Strategy. This uses many different types of investments, to give your money the opportunity to grow over the long term.

Cushon

Press releases

Cushon Mansion House Accord

Press comment